Home

Home

Published on

12 December 2022

Under the category

We explore the challenges FIs are facing in the race to comply with upcoming regulations, and the importance of leadership, culture and people in an ESG context.

A joint collaboration article with Fenergo.

Operationalising ESG: what is it and where do you start?

ESG is now a major force in financial services, with its criticality only set to increase as

more jurisdictions adopt regulations and standards. With the implementation of

SFDR and CSRD, the EU has led the charge in making ESG considerations a key

part of Client Lifecycle Management. 97% of banking executives[1] say that sustainable digitisation is key to success – but what does ESG mean to

your organisation? With so many standards available from TCFD to UNGC to ISSB

and beyond, how does a financial institution design and operate an ESG process

that delivers compliance without impacting the end customer experience?

Why operationalising ESG is important.

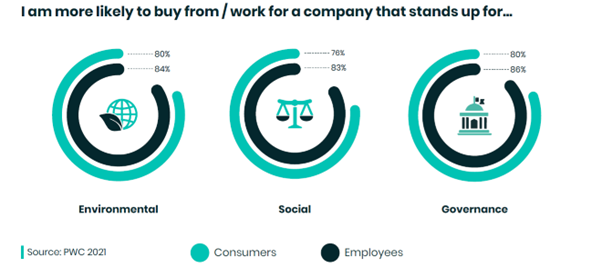

Recent polling shows that six in 10 (59%) of financial institutions are unsure if their organisation is equipped to meet ESG requirements[2]. With a spate of fines and incidents of greenwashing, this is a major point of exposure for financial institutions. More and more, consumers and employees expect the firms they do business with to embody ESG values – the reputational impact of positive ESG activity delivers dividends for financial institutions. But ESG is not just a cost; it can also be a revenue driver. With capital requirements leniency (such as Article 501a) and the opportunity to offer new, sustainability-focused products, ESG can attract forward-thinking customers treating it as a priority.

In this first of two articles, we explain how you can ensure your organisation is not left behind as ESG comes into force. We’ll discuss how a strategic approach can deliver for you and your clients, and what you need to consider from a people, policy, and process perspective.

What does it mean to be compliant with ESG?

This varies per jurisdiction and per financial institution, as each has their own risk appetite, regulatory environment, and view of the market. But the fundamentals are the same; regulatory obligations such as the EU’s SFDR and CSRD are coupled with the application of due diligence standards to understand the client profile.

Meeting regulatory obligations is not easy, but it is straightforward; the legislative text is black and white, and applicable scoping is clear. However, with over 400 standards available, how does an FI decide what standard to adopt, and how to implement it. There has been a level of maturation in the space, with key standards TCFD and the upcoming ISSB being widely adopted by jurisdictions (such as the UK and Thailand) and firms. That said, standards are guidelines and not binding; each FI must forge their own policy according to their risk appetite and market perspective.

Make it central to your strategy and culture.

To operationalise ESG successfully, there needs to be a recognition that ESG must extend beyond just regulatory compliance. Instead, a genuine shift in corporate mindset needs to occur to incorporate ESG into the culture of financial institutions and avoid corporate hypocrisy visible to both customers and employees. There is a strong link between employee perception of corporate hypocrisy and work engagement, where if an employee views inconsistencies between their company’s actions and their communication, there is a decrease in the dedication to their work[3]. This disengagement is likely to filter through to negatively impact customer trust, attraction and retention. As a result, integrating ESG into the corporate culture and business model is critical to its successful operationalisation and can generate added financial value[4]. Internal communications should clearly define their commitments, goals, and path to achieving them, whilst external communications should be transparent and unambiguous.

FIs must also assess the industries they want to continue servicing in a new ESG context. There is a growing need to phase out industries which pose a significant environmental or ethical risk. For example, HSBC created a target of Net Zero by 2050, and HSBC Asset Management have committed to phasing out the financing of coal-fired power and thermal coal mining by 2030 within the EU and OECD. This move away from servicing non-renewable energy firms that don’t take sufficient action to reduce carbon emissions is a major step by a Tier 1 bank. Other FIs have joined HSBC in their commitment to phasing out financing of coal by signing the Powering Past Coal Alliance at the COP26 summit. This could be the first step for FIs to shift away from financing polluting industries.

A recent report confirmed that in 2019 the largest global banks invested over USD 2.6 trillion in sectors that are primary drivers of biodiversity destruction[5]. Industries such as metal and mineral mining could be next to be phased out as public pressure grows for FIs to take accountability for environmental damage caused by their lending. FIs that focus early on environmentally friendly industries will reduce reputational risk, service a growing customer demand, and gain a competitive advantage. Formal regulations may emerge in the coming years, but the creation of internal policies and procedures around servicing environmentally harmful industries would enable FIs to get ahead of the curve.

Expertise and streamlined, effective processes will be key to successful operationalisation of ESG.

People are a key component to successfully integrating ESG. Training investment teams to advise on ESG-related products will increase customer access to sustainable finance and analyst insights into a poorly understood space. There is a growing consumer appetite for ESG-related products. In a recent study of asset managers, 38% of respondents think that a stronger focus on ESG factors in their investment approaches will improve returns[6]. By training Front-office teams, FIs can meet customer demand for ESG-aligned assets and potentially gain increased wallet over rivals who have delayed their ESG integration.

In the back office, incorporating ESG into existing processes as opposed to independent checks can generate efficiencies and avoid fragmented procedures. There is a strong overlap between ESG and CDD/KYC practices for the collection of data. Subsequently, ESG risk analysis can be integrated into every stage of the risk management framework by uplifting the due diligence process with ESG requirements, resulting in a more holistic risk model[7]. This will allow FIs to identify potential risks and mitigate them through exclusion policies or adapted risk premiums.

Collecting ESG related information in an independent process can be time-consuming and costly due to the difficulties in obtaining accurate data. Instead, existing CDD/KYC data can be reused, and teams upskilled by enhancing their training for specialist/complex clients, with ESG-MLRO type teams who deal with escalations. The depth of the process integration is entirely up to FIs. The most optimal operating model is still a matter of active discussion and it’s likely that a tailored ESG approach is required for each organisation due to the differences in structure and strategy.

Case Study

Data and Automation

ESG is a broad church, covering not only the sustainability credentials of the client, but also their suppliers (so called Scope 3 emissions). The scope of information that needs to be captured, validated, and fed into the ESG rating necessitates a comprehensive data strategy. The first step is to define a policy, usually an institution-specific amalgamation of key standards like TCFD and IISB.

Once the policy is agreed, the next step is to determine how the data will be captured. There are several options here:

- Re-use existing KYC data where there is an overlap for things like Nature of Business, Industry Codes, Board of Directors, etc.

- Reach out to the market for public data on larger corporate clients

- Outreach to the client either directly, or through self-serve client portals

When selecting a market data provider (or multiple providers), it is important that minimum criteria of quality and granularity are maintained. This means sourcing data that is verified and quantitative, rather than subjective, qualitative assessments of ESG performance. For this reason, larger FIs will tend to forego reliance on external rating providers (which are often the same firms as data providers), in favour of generating their own data-backed, traceable rating. This is due to the opacity of many rating methodologies, and the huge rating score variance between different providers for the same entity.

Where market data is not yet available (i.e., smaller private companies), the process becomes one of outreach; how best do we request data from clients and fulfil the ESG requirements.

As with data, the process of ESG has the potential to be labour-intensive and slow. Completed manually, ESG requires a lot of personnel. Even if a financial institution were willing to hire a team of (pricey!) ESG specialists to complete the due diligence, they will struggle to get them. ESG specialists are thin on the ground.

For reasons of cost, resource availability, and most importantly client experience, successfully implementing ESG depends upon automating processes where possible and appropriate. We cannot create an operational issue while solving a compliance one, making automation a must-have up front.

As touched on above, data can be automated by re-using data and leveraging external data providers. The provenance of data is also crucial. We don’t want to pull in information of questionable quality of source.

From a process perspective, automation extends to the automated screening of Controversial Activities. Like Adverse Media for AML, Controversial Activity looks at the news stories around the client to determine the presence of incidents that would affect the ESG rating. These can be automatically resolved where they are low relevancy or materiality, saving on manual effort.

Ratings themselves can be automatically calculated, with the option of conditional reviews for unusual clients or tricky segments (e.g., uranium mining or ammunition manufacture). Overall client reviews can similarly be automated, where well-performing clients are automatically accepted, and only unusual or poorly rated clients escalated for review.

By embedding automation in the ESG process, financial institutions can deliver regulatory compliance and a deep client understanding without sacrificing customer experience and lead times.

Case Study

Anorak Finance* were an early adopter of ESG, defining an ESG policy in 2021 and rolling it out as part of their standard onboarding process. However, they quickly realised that they faced an operational issue when it came to ESG – they were achieving compliance, but the due diligence effort was damaging their lead times and ultimately the customer experience. Staffing costs were also rising as more entity types and regulations came into scope

To address this, Anorak took three main actions. Firstly, ESG was ‘brought in from the cold’ and made part of existing CLM processes, rather than a standalone activity. This brought efficiencies by re-using teams. Secondly, they brought in market data providers which drastically cut down the effort to complete due diligence on larger corporates and publicly listed companies. Finally, processes in screening, risk, and approvals were automated for highly-rated and low-risk clients so that teams could focus on more complex customers.

By automating in a diverse fashion through a mixture of services, internal processes, and operating model, Anorak were able to address their OpEx challenges and transform the customer experience.

*Name omitted

Key takeaways:

- Get on top of evolving regulations and forge a policy according to the firm’s risk appetite and market perspective

- Go beyond compliance – lead from the top with a clear communication strategy and action plan

- Consider ESG as an opportunity for differentiation and growth, not simply a cost or compliance burden

- Invest in your teams for long-term benefits and returns

- You don’t necessarily have to reinvent the wheel – engraining ESG across the CLM journey can ensure compliance without negative impact to the customer

- Re-use existing data and leverage the existing data provides that you trust

- Leverage technology for rating calculations and client reviews, so you can focus on the high risk clients

If you'd like to learn more about how you can successfully operationalise ESG, get in touch at enquiries@AuroraSDE.com today.

References:

[1] Censuswide:

Benchmark for Sustainable Banking Report 2022

[2] Operationalising ESG: Turning a Regulatory Obligation into a Market Opportunity

[3] Consistency or Hypocrisy? The Impact of Internal Corporate Social Responsibility on Employee Behaviour: A Moderated Mediation Model

[4] ESG Colourwashing: Combating Modern-day Corporate Hypocrisy

[5] Portfolio Earth Jan 2021

[6] PwC ESG Transformation July 2021

[7] Six

key challenges for financial institutions to deal with ESG risks